Tom Werner

Intro

Citi Trends ( NASDAQ: CTRN) shares have actually fallen 39% YTD. Regardless of the reality that the business is not valued extremely by multiples, I think it is still not the very best time to go long.

Financial investment thesis

In my individual viewpoint, in the next quarter, we will see ongoing pressure from traffic in the shops of the network and the typical look at the development rate of business’s profits, which will likewise add to press on success due to the deleveraging impact. I think that the weak trading patterns in 2Q and the absence of clear advantage drivers might continue to moisten the stock’s essential advantage capacity. Nevertheless, the business is presently not valued extremely, and a prospective modification in the macro environment might have a substantial effect on target customers and, as a result, the monetary outcomes of business in the future, so I abide by the HOLD suggestion, not the Offer suggestion. Personally, I see the business as an outstanding bet genuine non reusable earnings development amongst low-income individuals.

Business introduction

Citi Trends is a worth merchant of garments and devices. The business’s target market is individuals with an earnings of less than $25,000 each year. The primary sales channel is the offline format. The business runs in the United States market. According to the outcomes of the first quarter of 2023, the business has 608 shops in 33 states.

1Q 2023 Incomes Evaluation

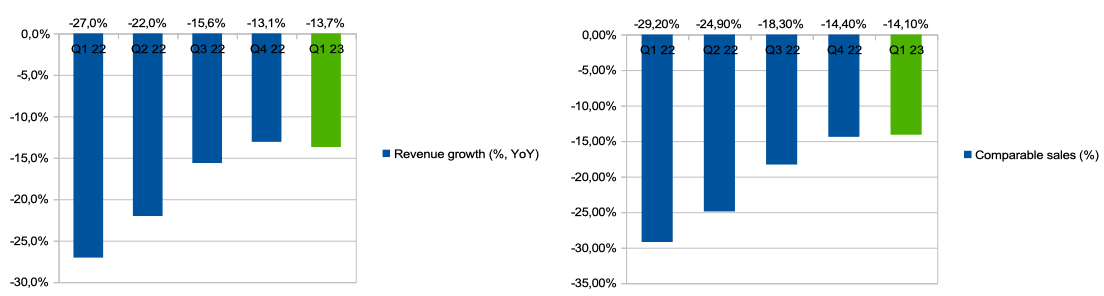

According to the outcomes of the first quarter of 2023, the business’s profits reduced by 13.7% YoY and reached $179.7 million. As the primary factor for the decrease in profits, I would single out the ongoing decrease in equivalent sales by 14.1% YoY as an outcome of macro headwinds pressure on the business’s customers. We see that the business is dealing with both a decline in traffic in the shops of the network and a decline in the typical check. You can see the information in the chart below.

Business’s information (Business’s information)

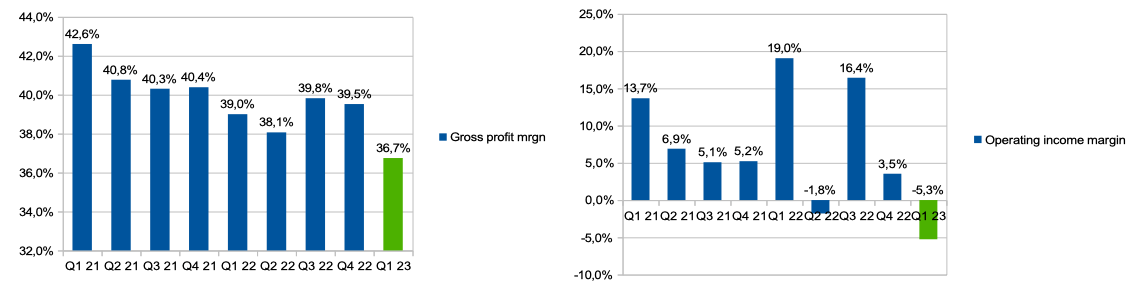

Gross margin likewise reduced from 39% in 1Q22 to 36.7% in 1Q23, and running margin reduced from 19% in 1Q22 to -5.3% in 1Q23 as an outcome of the deleveraging impact, due to which the share of costs on SGA (% of profits) increased from 34.1% in 1Q22 to 39.4% in 1Q23. The primary factor for the deleveraging impact is the reality that the majority of the business expenses are repaired (lease, incomes), as an outcome, we see pressure on running success while decreasing organization volumes.

Business’s information (Business’s information)

Customer costs on clothes amongst the business’s target market is incredibly conscious the enhancement or degeneration of the macro environment, as the business concentrates on customers whose earnings does not surpass $25,000 each year. At the minute, we see that equivalent sales drag equivalent business in the market that run in a comparable sector. In the table listed below you can see a contrast of Q1 2023 equivalent sales in between City Trends, Ross Stores ( ROST), and TJX Business ( TJX), where I utilized just the United States department.

Business’ details (Business’ details)

The business is still debt-free, with money and liquid properties on the balance sheet for 1Q2023 at $164 million, which is incredibly favorable, as the existence of a monetary cushion and the lack of financial obligation are specifically crucial consider an environment of weak trading patterns.

My expectations

Based Upon management’s remarks throughout the Incomes Call following the business’s Q1 2023 report, we can conclude that early Q2 trading patterns follow a weak Q1 2023. Hence, the business’s sales in April are at the level of the lower bar of the business’s expectations, which remains in line with the formerly revealed assistance on a decline in profits in the series of unfavorable mid-single-digits to unfavorable low-single-digits as compared to financial 2022. The management likewise clarified that the pattern continued in May.

I think we will see expectedly weak outcomes for 2Q 2022 as the pressure on profits development will, in my individual viewpoint, continue to add to the deleveraging impact due to the high share of repaired expenses for lease and salaries.

Likewise, based upon my own expectations, basic financial patterns and remarks from the business’s management, I can make a presumption that we can see an enhancement in monetary efficiency in the 2nd half of 2023 as macro headwinds stabilize. I wish to repeat that the business’s target market is customers with an earnings of less than $25,000 a year, who are especially conscious increasing expenses of living, increasing rates and raised inflation.

Dangers

Earnings development & & margin: continued decrease in traffic in the chain’s shops and a decline in the typical ticket might lead not just to a more reduction in profits compared to 2022 however likewise to a decline in economies of scale, which might add to press on success. In addition, the business runs in the retail organization, where the level of repaired expenses (lease, wage) is fairly high, so a decline in organization volume can cause a deleveraging impact.

Macro: the business’s target sector is customers, which are especially conscious increasing item rates, so a decrease in genuine earnings due to high inflation might have an unfavorable effect on both organization development and running margins.

Chauffeurs

Margin: the business is presently dealing with the production and launch of a brand-new ERP system that will assist handle stock in storage facilities more effectively. Hence, the launch of a brand-new ERP system that will change the old one can cause a boost in running success by decreasing operating expense. In accordance with the remarks of management, the launch of the system will occur at the end of summertime 2023, nevertheless, we will probably see any substantial outcomes and effect of the brand-new system on monetary declarations just in 2024.

Macro (basic motorist): the healing of customer self-confidence and the development of genuine non reusable earnings of the population can have a substantial effect on customer habits, while the development of traffic in the chain’s shops and the development of the typical check can supply substantial assistance to profits development. In my viewpoint, a business’s organization design that depends on customers with earnings of less than $25,000 is specifically conscious altering macro conditions.

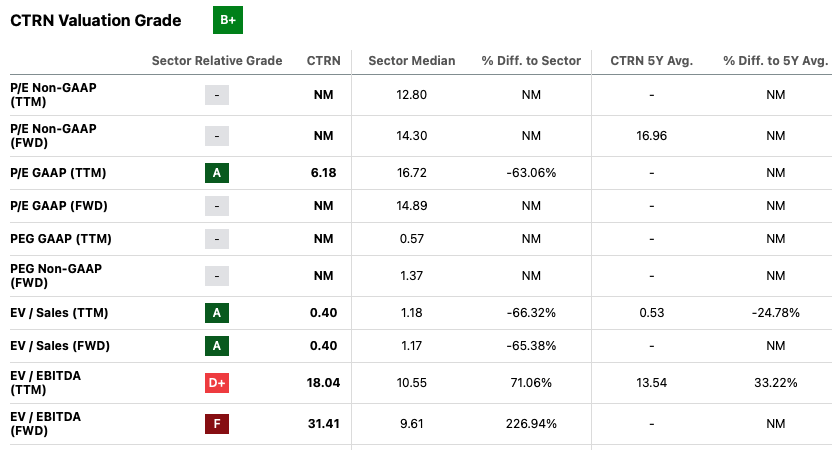

Appraisal

At the minute, in my viewpoint, the business is inexpensively priced relative to its historic level. I think that the marketplace considers the threats that as the macro scenario enhances, customers might “take their time” to increase the typical check and increase the frequency of going to the chain’s shops. In addition, there is still a danger that macro headwinds will continue to have an unfavorable effect in the 2nd half of 2023.

Appraisal (SA)

Conclusion

Hence, I wish to keep in mind that at present the business is under pressure on monetary efficiency due to a weakening customer, which is extremely conscious modifications in macro conditions, and the business’s organization design indicates pressure on success with a decline in organization volumes due to repaired expenses.

I think that trading patterns in Q2 2023 will resemble Q1 2023, which is certainly not a favorable element for stock rates. Nevertheless, I will continue to carefully keep track of the business’s monetary declarations for Q3 and Q4 2023 and any signals of normalization in customer habits amongst the business’s target market. In the meantime, I’m adhering to HOLD’s suggestion, nevertheless, I more than happy to alter my suggestion to Purchase as I think the business is an outstanding bet to enhance macro conditions and their effect on the target market of business.