DNY59

The deeply inverted bond yield curve and the raised yield on inflation-linked bonds make this a good time to purchase the Quadratic Rates of interest Volatility and Inflation Hedge ETF ( NYSEARCA: IVOL) to gain from yield curve steepening and/or decreasing genuine bond yields. The IVOL likewise provides a method to hedge versus a decrease in equity market threat.

IVOL is a fixed-income ETF that holds a portfolio of inflation-linked bonds and alternatives that looks for to hedge versus a steepening yield curve, whether from falling short-term rate of interest or increasing long-lasting rate of interest. The bulk of the IVOL’s properties are kept in the Schwab U.S. SUGGESTIONS ETF ( SCHP) which holds inflation-linked bonds with a typical maturity of 7.4 years, which gain from increasing inflation expectations. The rest is kept in OTC alternatives which look for to gain from yield curve steepening, especially the spread in between 2-year and 10-year rates of interest swaps. The chart listed below demonstrate how the IVOL has actually been carefully associated with both the SCHP and the 2s-10s spread because its creation in 2019.

IVOL Vs SCHP and 2-10 Yield Spread (Bloomberg)

The IVOL has actually had a ghastly time over current years as short-term rates have actually risen greater, with the ETF losing over 20% over the previous 2 years. The collapse in the yield curve has actually seen the IVOL underperform the SCHP substantially due to the losses seen on its alternatives. The high cost ratio of 1.03% has actually likewise functioned as a drag.

A Turnaround Is Growing Most Likely Every Day

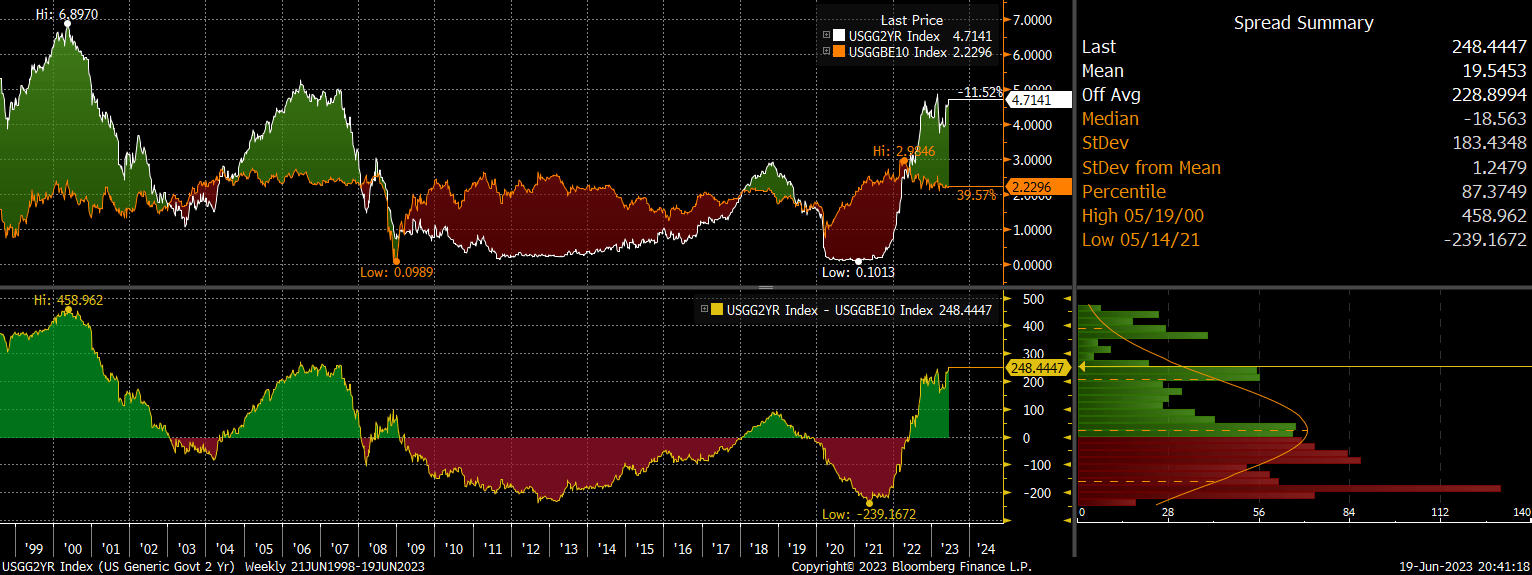

Nevertheless, conditions are now complimentary for the IVOL. To start with, the genuine yield on the SCHP has actually increased to 1.5%, which is substantially above its long-lasting average and is far too expensive in the context of high financial obligation levels. Second of all, the spread in between 10- and 2-year bond yields is incredibly unfavorable. The mix of an inverted yield curve and high 10-year genuine yields implies that 2-year rates are now incredibly raised relative to long-lasting inflation expectations. The spread in between 2-year yields and 10-year inflation expectations is now a lofty 2.5%, and the IVOL is basically a bet on this spread moving lower.

Spread of 2-Year UST Yield and 10-Year Breakeven Inflation Expectations (Bloomberg)

2 Bullish Macro Circumstances

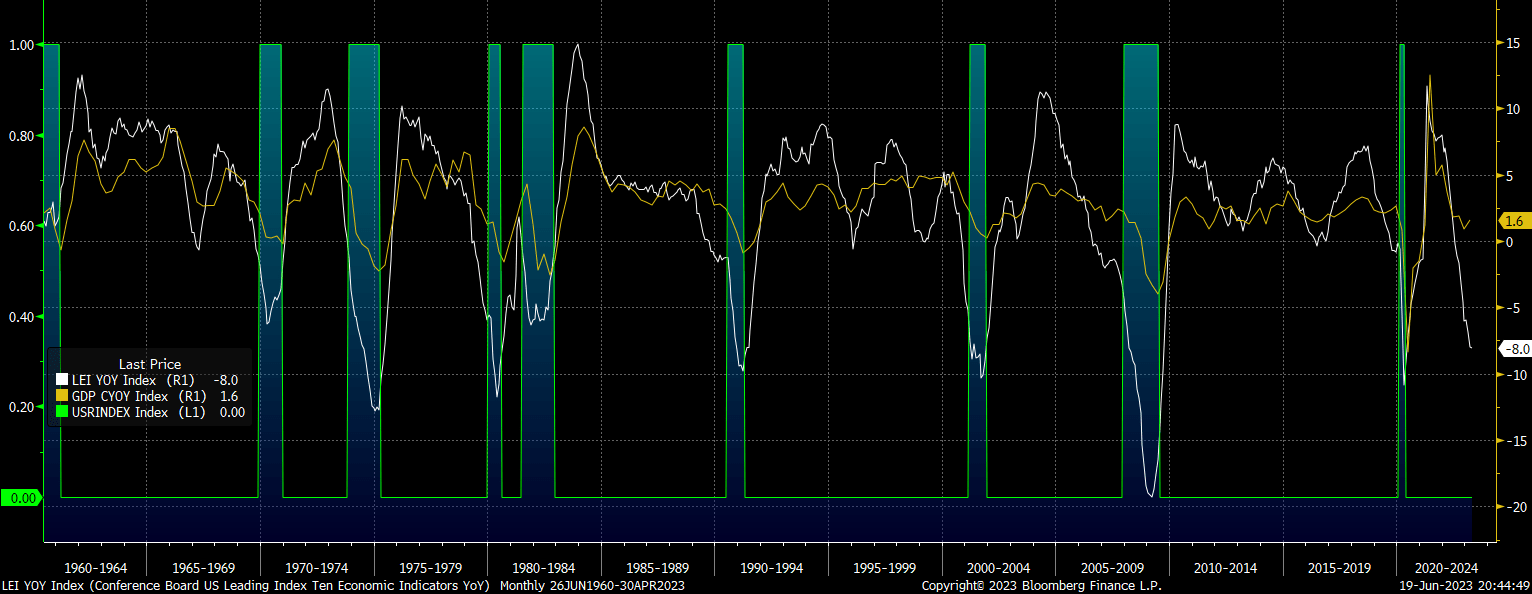

I see 2 primary macroeconomic situations that might drive a healing in the IVOL, keeping in mind that we are more than likely to see some mix of the 2. One is that we see a sharp drop in short-term rates as we get in economic downturn. Leading financial signs continue to indicate an economic downturn, with the Conference Board’s Leading Economic Index now down 8.0% y/y, which has actually never ever been seen beyond a main economic downturn.

Leading Indication Development Vs Real GDP And NBER Specified Economic Crises (Bloomberg)

While this would likely trigger losses on the IVOL’s SCHP holdings as inflation expectations tend to fall throughout an economic downturn, the ETF would gain from a sharp steepening in the yield curve. The 19% rally in the IVOL in the middle of the sharp drop in short-term rates that arised from the local bank failures in March highlighted the degree to which the IVOL can rally on yield curve normalisation.

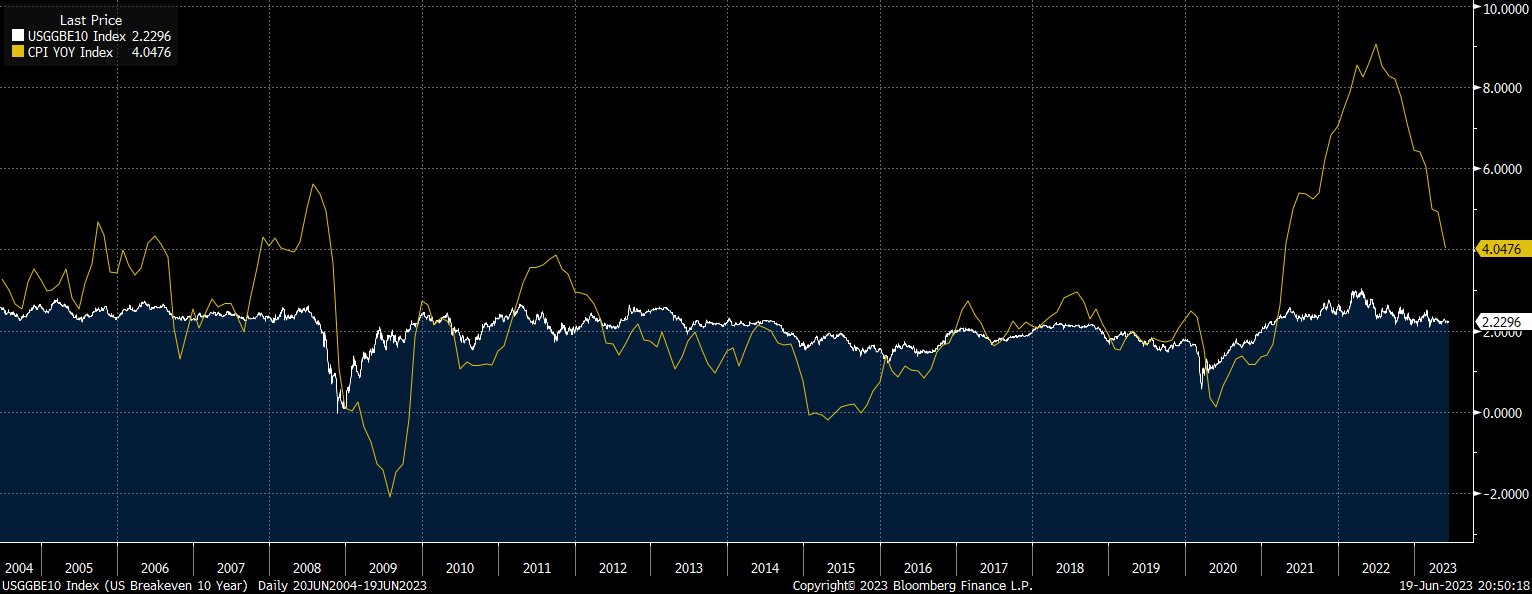

Another situation is that we see a healing in inflation expectations, which would increase the IVOL’s SCHP holdings and likewise put upside pressure on long-lasting yields to the possible advantage of its alternative holdings. 10-year breakeven inflation expectations sit at simply 2.2%, which is a long method listed below heading CPI of 4.0% and the 10-year average of 2.7%. An increase in product rates is one possible trigger that might trigger bond market financiers to anticipate existing raised inflation to continue.

10-Year Breakeven Inflation Expectations Vs CPI (Bloomberg)

Main Danger Originates From Continued Equity Market Gains

The primary threat to the IVOL ETF originates from an extension of the patterns in location over the previous year, with short-term rates continuing to increase even as inflation pressure decreases even more. The speed of the rate walkings integrated with the collapse in cash supply in the middle of quantitative tightening up has actually led bond financiers to prepare for a drawn-out reducing cycle, keeping the yield curve inverted. With the yield curve now at its most inverted level because 1981, and the spread of 2-year rates over cash supply development at record lows, there is a limitation to just how much longer the Fed can keep rates raised prior to we see a credit crunch.

Nevertheless, one crucial threat is that the current rally in United States innovation stocks continues, requiring the Fed to preserve extremely limiting policy to attempt to avoid another stock mania as we saw in the late-1990s. 2-year bond yields increased to a peak of 6.9% in 2000 prior to the tech bubble burst, lastly enabling rates to return down in line with the genuine economy, and a repeat of this would trigger considerable losses for the IVOL. Choices agreements likewise have actually embedded utilize because the financier’s general direct exposure to the underlying technique that the alternatives are based upon is higher than the worth of the alternatives. However, I think that now is a good time to get direct exposure to the IVOL from a tactical viewpoint, and an especially great time to utilize it as a hedge versus stock exchange decreases.