Summer Season is here, and real estate stock is lastly growing! The spring real estate stock resembled a zombie increasing from the tomb, really sluggish, however the summertime is revealing some pledge and let’s hope it continues. Purchase apps had a little week-to-week gain. Home mortgage rates were once again in a little variety, hanging near 7%.

Here’s a fast rundown of the recently:

- Active stock grew 8,886 weekly. I am still wishing for some weeks that reveal stock development in between 11,000-16,000

- Home mortgage rates remained in a tight variety in between 6.875% -6.95%

- Purchase application information revealed a 2% development week to week

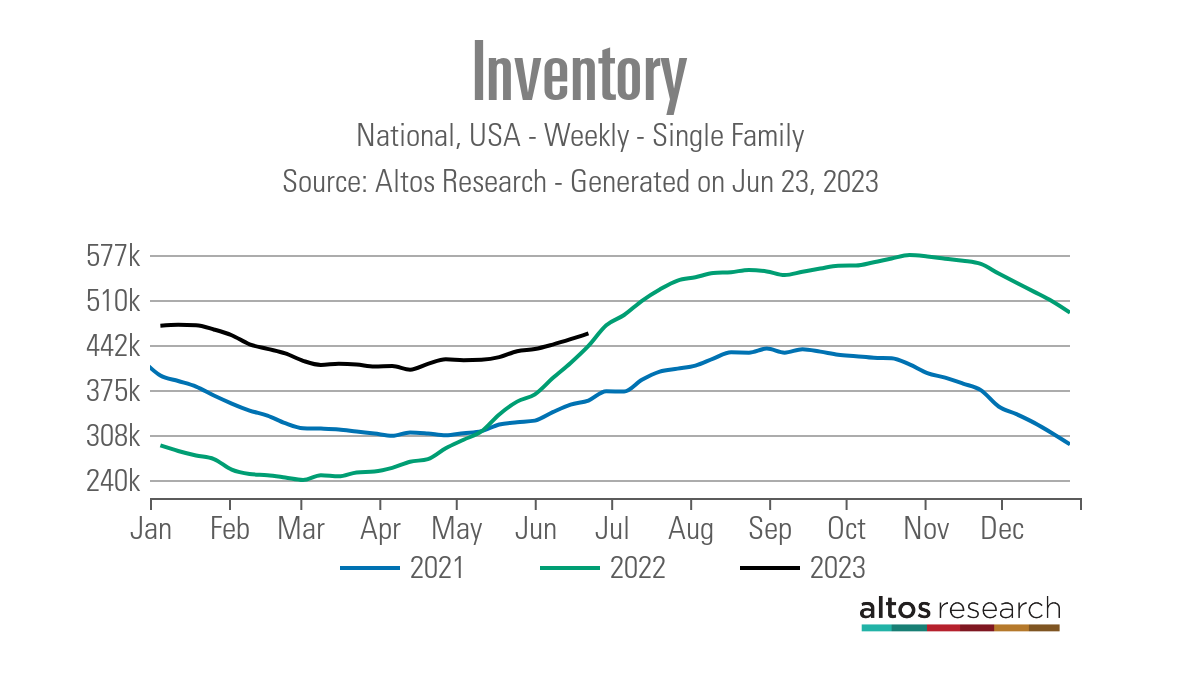

Weekly real estate stock

The active listings information saw good development recently, less than I want to see, however development however. I would feel better about the stock circumstance if we included an extra 3,000-8,000 homes to the weekly information line from existing levels. Nevertheless, the genuine favorable story here is that even with brand-new listing information trending at an all-time low, we are getting the development in active listings we typically see in the spring and summertime.

- Weekly stock modification (June 16-23): Stock increased from 451,047 to 459,907

- Very same week in 2015 (June 17-24): Stock increased from 415,582 to 441,106

- The stock bottom for 2022 was 240,194

- The peak for 2023 up until now is 472,680

- For context, active listings for today in 2015 were 1,179,728

As you can see in the chart below, the stock development has actually been sluggish this year, and we will have unfavorable year-over-year weekly active stock information soon. However, in 2015 saw the most significant house sales crash ever taped in history, so the increase in stock in 2015 took place since of an irregular occasion and we were working from a really low bar. So, it should not be a shock that as quickly as real estate need simply supported, we faced some unfavorable year-over-year information.

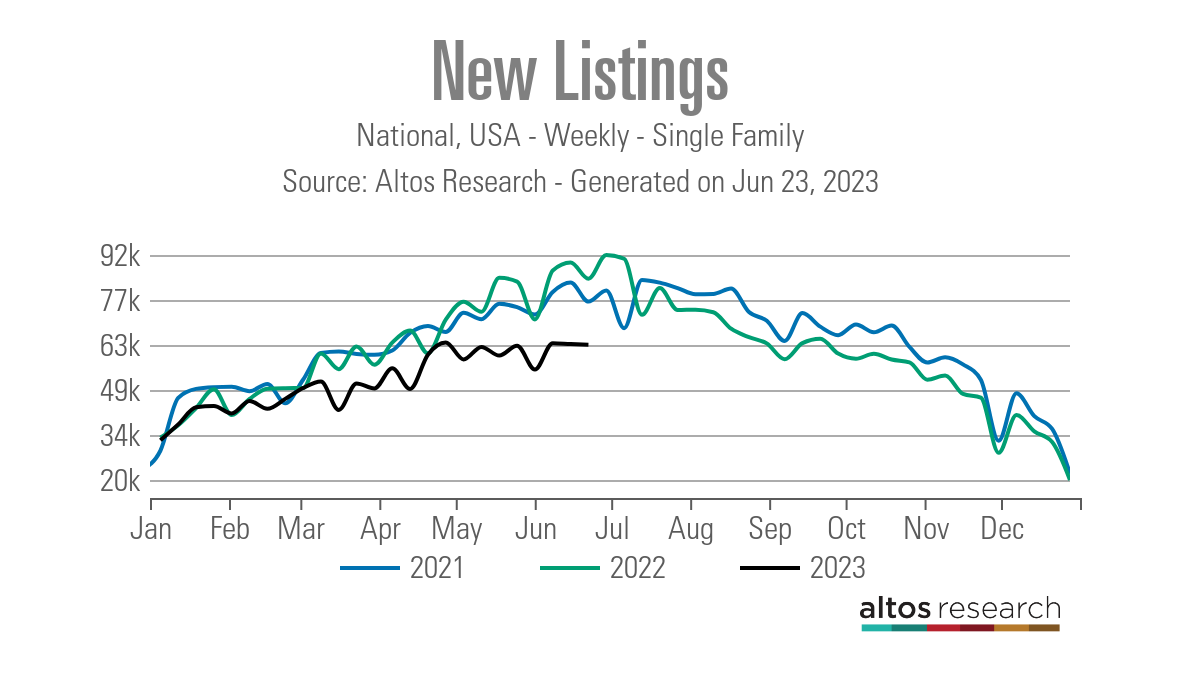

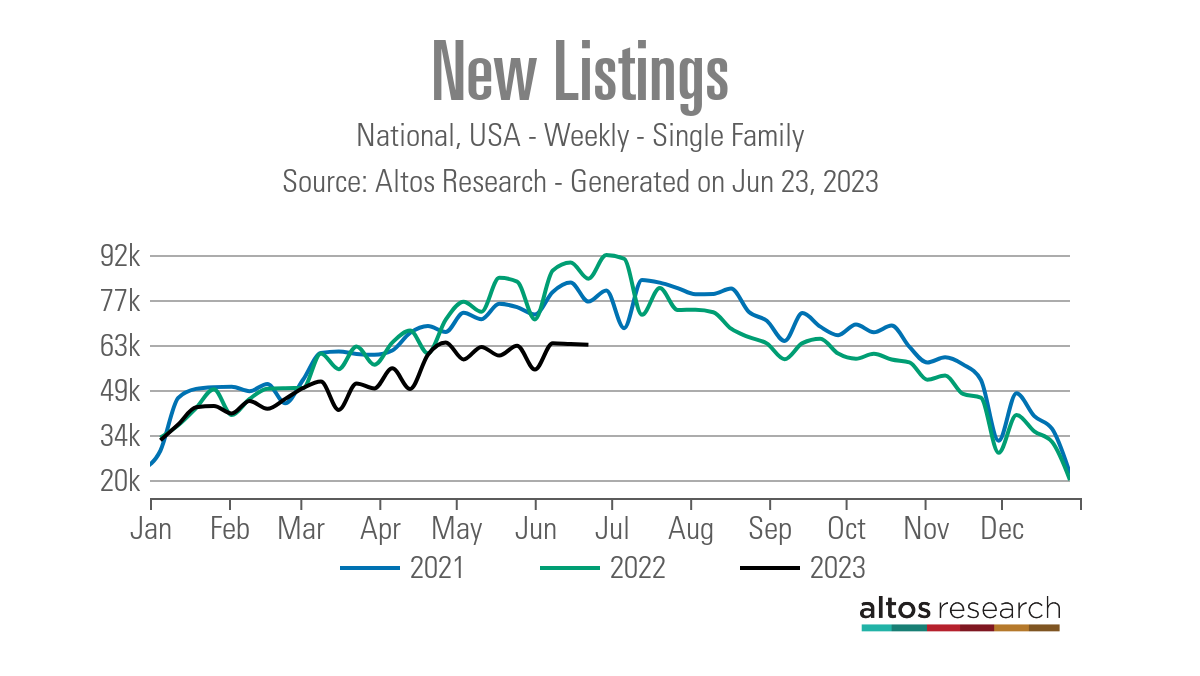

In addition, brand-new listing information turned unfavorable year over year after the 2nd half of 2022. The cost struck with greater home loan rates has actually affected brand-new listings information because a lot of sellers are purchasers, therefore assisting in an all-time low in brand-new listings information. Likewise, we should keep in mind that even in 2021, when we had 3% home loan rates, brand-new listing information was trending at lowest levels.

New listings information has actually had 3 weeks in a row of unfavorable weekly information, absolutely nothing huge, obviously, however we are beginning to enter into the seasonal decrease duration of this information line. This is something to concentrate on over the next 4 to 6 weeks. The information reveals a visible decrease year over year, and 2021/2022 were currently working from lowest levels.

Compare the brand-new listings information today to that over the last few years:

- 2023: 63,106

- 2022: 84,014

- 2021: 76,761

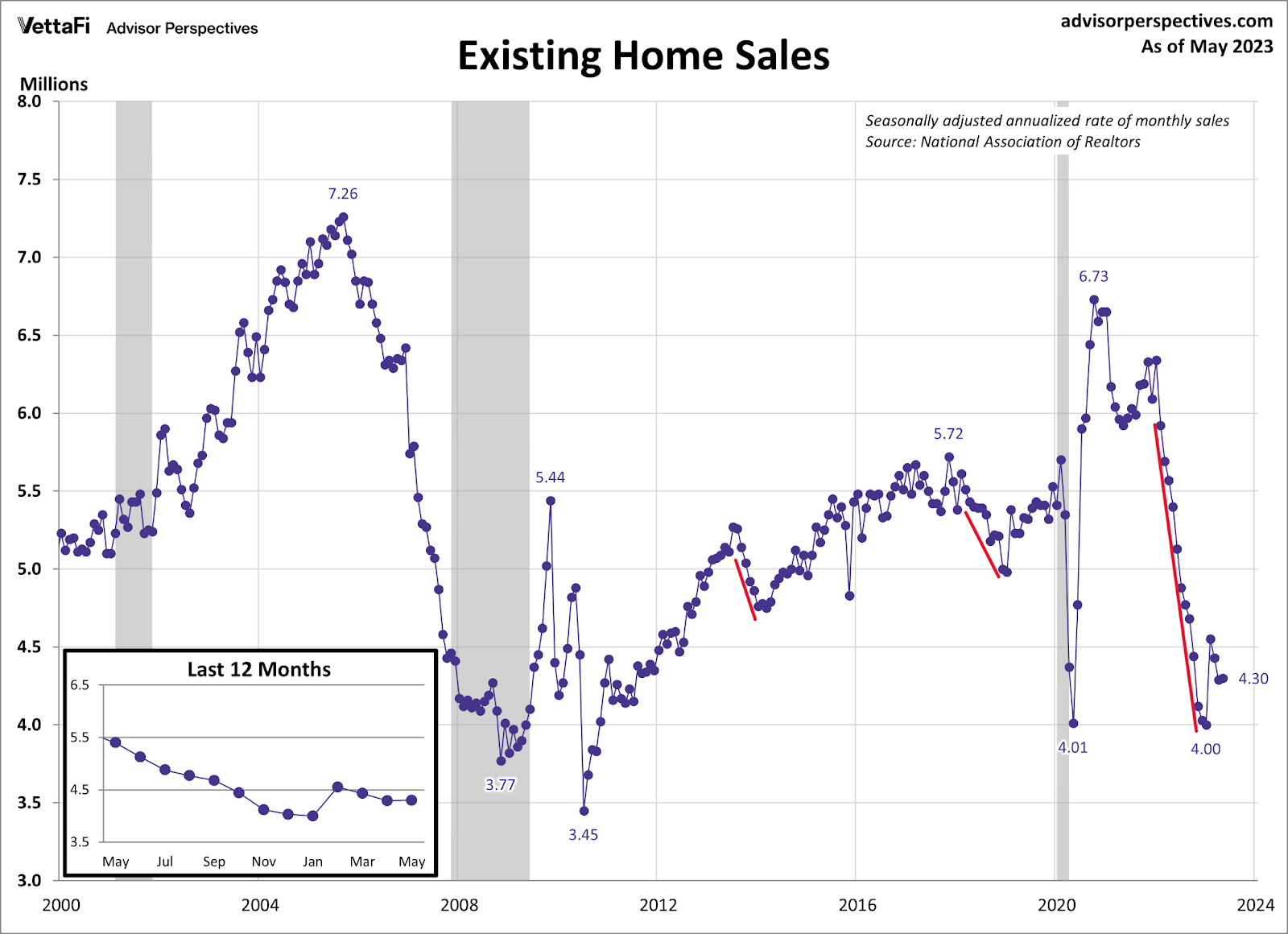

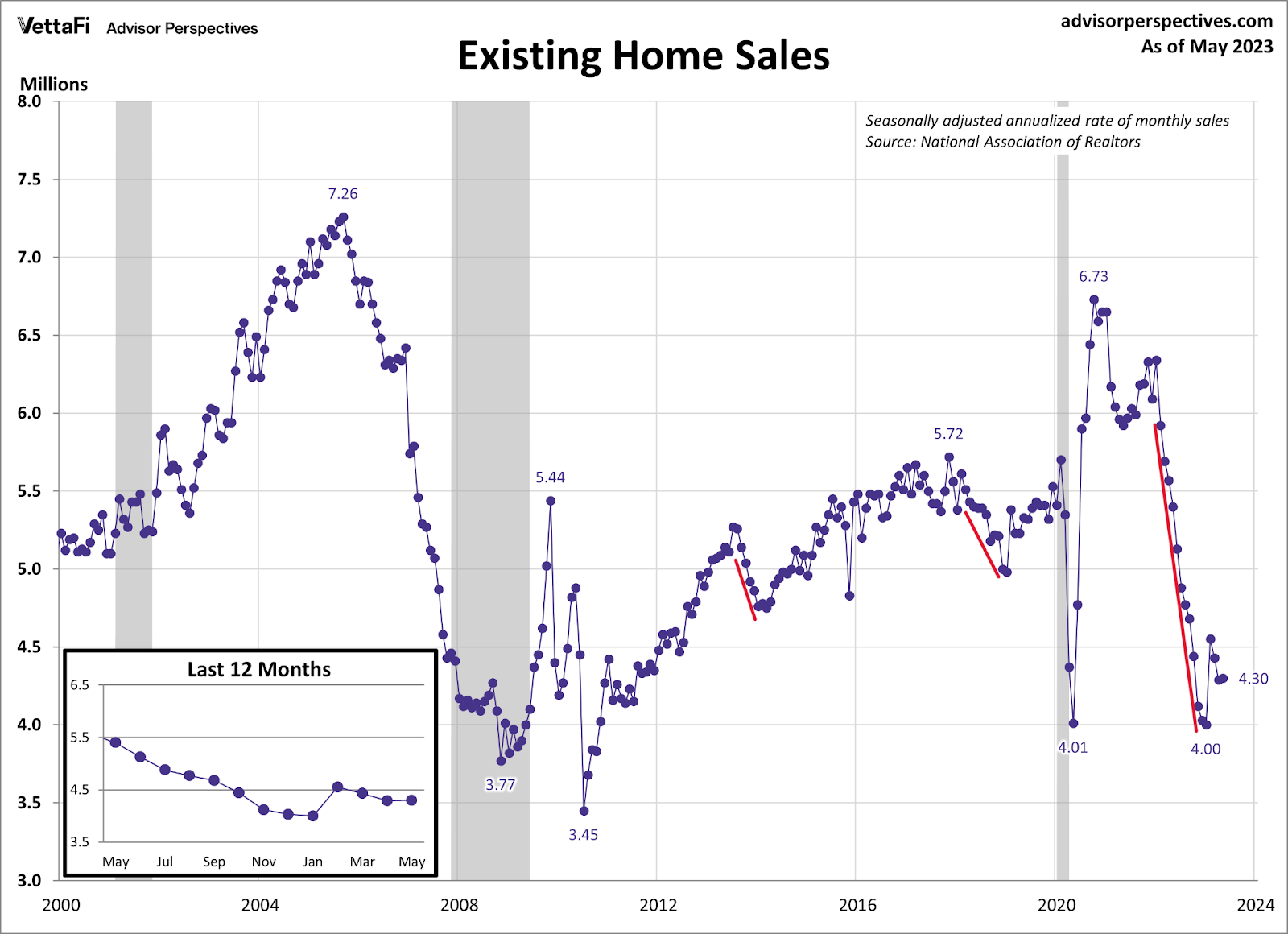

Recently, NAR launched the existing house sales report, which revealed a minor month-to-month development in sales. More notably, it revealed that the days on market hung back to the teen level, which suggests we are as soon as again in a savagely unhealthy real estate market Absolutely nothing good is taking place in real estate when days on market are so low. Likewise, NAR upgraded its stock report revealing a year-over-year decrease in stock.

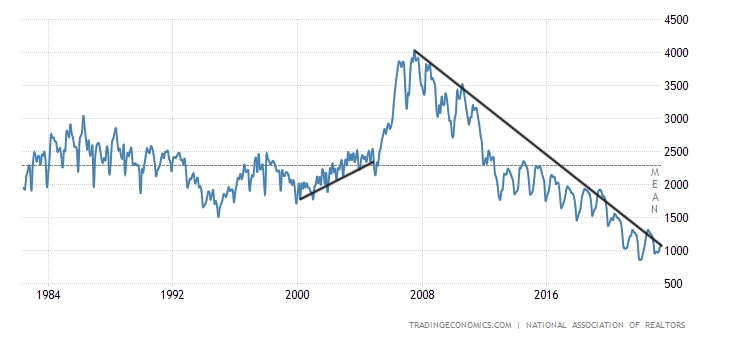

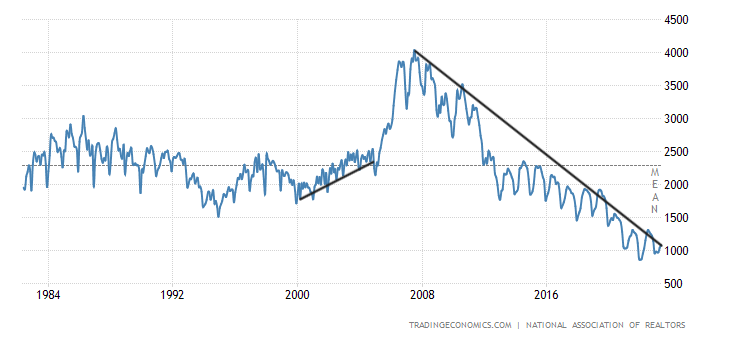

NAR overall Stock levels:

- Historically stock is in between 2-2.5 million

- The peak in 2007 was a bit over 4 million

- Presently we’re at 1.08 million

- In 2015 at this time it was 1.15 million

Individuals typically ask me why there is such a distinction in between the NAR information versus the Altos Research Study stock information. This link discusses the distinction and deserves a read.

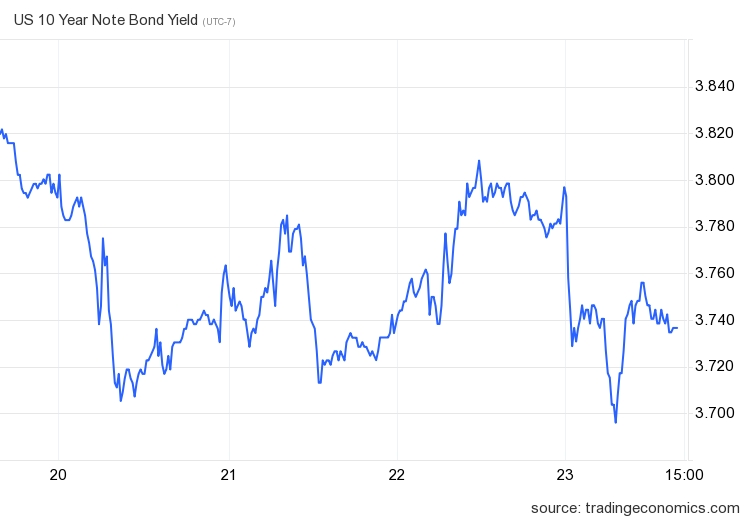

The 10-year yield and home loan rates

The bond and home loan rate world has actually been calm the last 2 weeks. Thinking about all the information and Federal Reserve talk we have actually had just recently, it’s unexpected how steady rates have actually been. The 10-year yield had a little variety recently, and home loan rates remained in a variety in between 6.875% -6.95%.

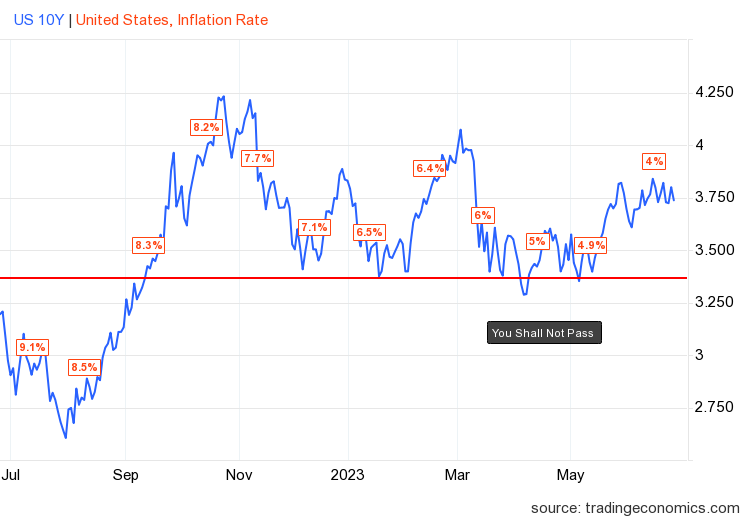

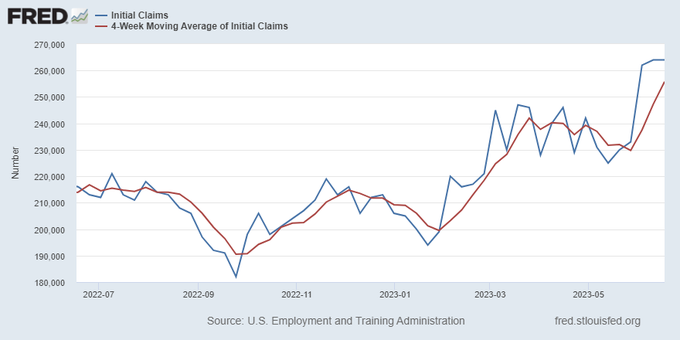

In my 2023 projection, I composed that if the economy remains company, the 10-year yield variety must be in between 3.21% and 4.25%, corresponding to home loan rates in between 5.75% and 7.25% As long as out of work claims pattern listed below 323,000 on the four-week moving average, the labor market remains company, which suggests the economy stays healthy. Out of work claims have actually remained listed below this variety all year up until now and task openings are still at 10 million.

I have actually likewise worried that the 10-year level in between 3.37% and 3.42% would be difficult to break lower. I call it the Gandalf line in the sand: “ You will not pass.” As you can see in the chart below, we have actually evaluated this line sometimes, and yet the 10-year yield might not pass. The setup for the 10-year yield to remain in the variety is undamaged. Unless the U.S. dollar blows up greater or we get some market tension overseas, we must stay in the projection variety.

The counter to my 10-year yield variety would be if the economy here or worldwide begins to speed up greater; that would be a legitimate facility to get the 10-year yield above 4.25%.

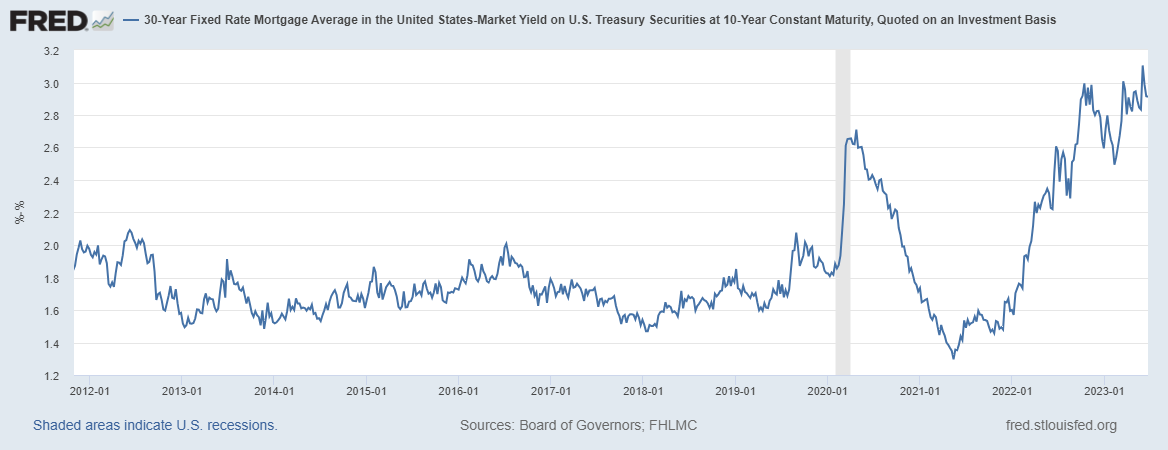

The problem in 2023 is more than the 10-year yield; because the banking crisis began, the spreads in between the 10-year yields and 30-year home loan rates have actually become worse, and up until the Fed sobs uncle, it does not appear like we will see anymore enhancement.

Another element of my 2023 projection is that if out of work claims break over 323,000 on the four-week moving average, the 10-year yield might break under 3.21% and head towards 2.73%. Recently we didn’t have much motion here with out of work claims, however we have actually seen the labor market get looser because the lows in 2022.

From the St. Louis Fed: Preliminary claims for joblessness insurance coverage advantages were little bit altered in the week ended June 17, at 264,000. The four-week moving average increased to 255,750

Purchase application information

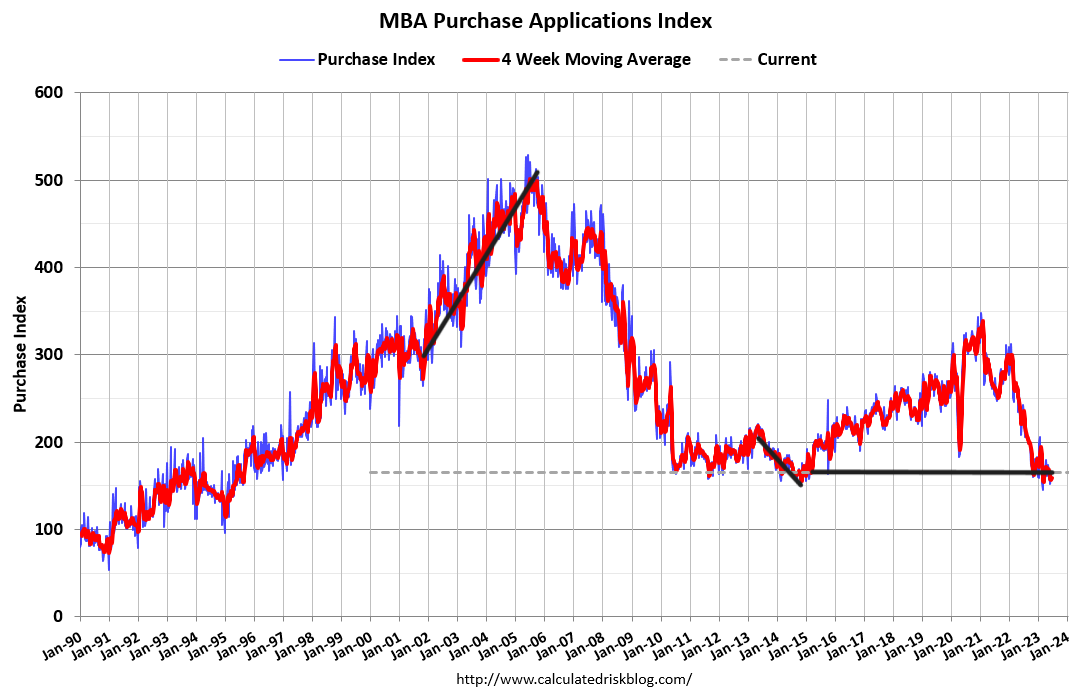

Purchase application information has actually amazed individuals with back-to-back favorable prints in the last 2 weeks of 8% and 2%, which suggests year to date, we have actually had 12 favorable prints versus 11 unfavorable prints. There is no clear instructions as needed on the week-to-week information. Nevertheless, the reality that this is taking place is a big offer, as you can see in the chart below. If this had not occurred, everyone would be having a various discussion today about the real estate market and stock.

Given That Nov. 9, 2022, we have actually had 19 favorable and 11 unfavorable prints, which reveals that need has actually supported. Now that we are nearly to July 4, you can plainly see it in the existing house sales information, as purchase apps are a positive indication.

House sales can still trend listed below 4 million this year if we see more weak point in purchase application information, however the sales decrease is much slower this year. This is substantial since the marketplace is acting usually once again with these low sales levels. This provides everybody a much better point of view of where need is going, as in 2015’s waterfall collapse was a historical occasion.

The week ahead: Real estate information and PCE inflation

We will have a huge week ahead in information. The S&P CoreLogic Case Shiller house rate index and the FHFA house rate index will come out today and they will reveal the tightening the month-to-month rate information compared to what we had in the 2nd half of 2022. Likewise, the brand-new house sales report is showing up, and we will see just how much development we have actually made.

Pending house sales will be out next week. I do not anticipate much to occur there; in reality, we might have an unfavorable report as we did have 4 straight weeks of unfavorable purchase application information just recently.

Likewise, the PCE inflation information will be launched Friday– this is where the Fed desires the inflation development rate to return down to 2%. I understand individuals enjoy to concentrate on CPI inflation information, however the PCE information matters more. Below is an appearance a Core PCE information, which the Fed wishes to see go much lower.

So, we have a hectic week of information, and obviously, we constantly watch out on out of work claims information every Thursday. Nevertheless, 4 real estate reports and inflation information with some Fed talk produce an amazing week for bond yields and home loan rates. Likewise, we never ever understand what we will receive from Russia, with love or without.