By Pam Martens and Russ Martens: October 16, 2023 ~

Jamie Dimon, Chairman and CEO of JPMorgan Chase

On Might 1, the Federal Deposit Insurance Coverage Corporation revealed that First Republic Bank had actually stopped working which it was being offered to JPMorgan Chase. At the time, JPMorgan Chase was currently the biggest and riskiest bank in the United States. The sweetie offer the bank received from the FDIC to take control of Very first Republic consisted of the FDIC consuming 80 percent of any losses on single-family domestic home mortgages for 7 years and 80 percent of any losses on industrial loans, consisting of industrial property, for 5 years. The FDIC likewise offered JPMorgan Chase with a $50 billion, five-year fixed-rate loan at a concealed rates of interest.

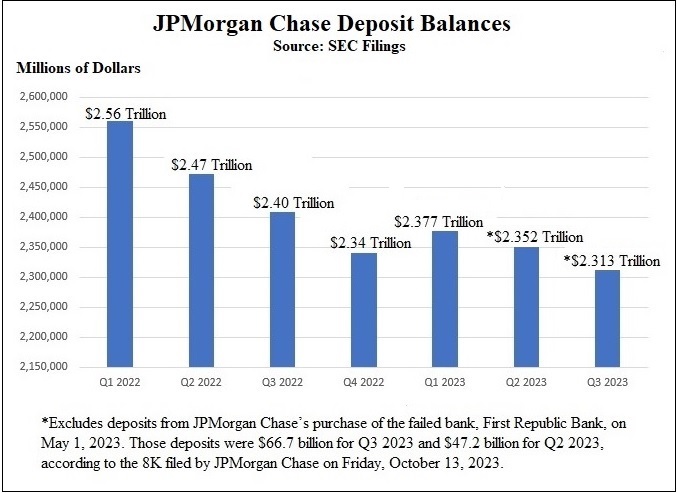

According to the filing that JPMorgan Chase made with the Securities and Exchange Commission last Friday, the offer likewise provided JPMorgan Chase something that it frantically required: deposits. According to the 8-K filing that JPMorgan Chase made with the SEC on October 13, the acquisition of First Republic Bank included $47.2 billion to its deposit base in the 2nd quarter and $66.7 billion in deposits in the 3rd quarter.

As the chart above shows, JPMorgan Chase suffered outflows of deposits in every quarter of 2022. It got a quick break from inflows of deposits in the very first quarter of 2023, as an outcome of the March banking panic that affected smaller sized banks, then outflows took hold once again. Leaving out the deposits from First Republic Bank, JPMorgan Chase has actually lost $248.38 billion in deposits over the period of the last 7 quarters. One does not anticipate that at a bank that continues to trumpet its “fortress balance sheet.”

Even consisting of the big quantity of deposits that JPMorgan Chase acquired from scooping up First Republic, the bank still bled $19.4 billion in general deposits in between the 2nd quarter of this year and completion of the 3rd quarter on September 30, according to JPMorgan Chase’s SEC filing on Friday, October 13.

Contributing to the look of desperation at JPMorgan Chase to support its deposit base, on September 28 Wall Street Journal press reporter Rachel Louise Ensign exposed that JPMorgan Chase was providing a shockingly high 6 percent interest on a 6-month certificate of deposit. There were 3 catches to get the offer: it needed to be brand-new cash originating from outside the bank; the minimum financial investment was $5 million; and the cash needed to be transferred by September 30. The date of September 30 simply takes place to be the last day of the quarter, the cutoff for the bank to report its last tally for deposits at quarter end.

There is something else impressive about that uncharacteristic spurt of kindness from JPMorgan Chase. By getting a minimum of $5 million in brand-new outdoors cash to get the 6 percent CD, the bank would seem successfully getting to grow its currently eyebrow-raising quantity of uninsured deposits. The FDIC guarantees deposits approximately $250,000 per depositor, per bank. The Wall Street Journal short article is quiet on how the balance of the $5 million would be safeguarded.

According to the bank’s regulative filings, since December 31, 2022, JPMorgan Chase Bank N.A. held $2.015 trillion in deposits in domestic workplaces, of which $1.058 trillion were uninsured The bank likewise held another $418.9 billion in deposits in foreign workplaces, which were likewise not guaranteed by the Federal Deposit Insurance Coverage Corporation (FDIC). That brought its uninsured deposits since year-end to an overall of $1.48 trillion or 60 percent of its overall deposits. (Under federal statute, the deposits held by U.S. banks that lie on foreign soil are not guaranteed by the FDIC. )

After the 2nd, 3rd and 4th biggest bank failures in U.S. history over the period of 7 weeks this previous spring, the FDIC has actually awakened to the threats of U.S. banks holding big quantities of uninsured deposits– whether they are uninsured due to the fact that they go beyond the $250,000 insurance coverage cap per depositor/per bank or are uninsured due to the fact that the deposits live on foreign soil. Big holdings of uninsured deposits added to the bank performs at Silicon Valley Bank and Signature Bank in March, which fell the banks and required an FDIC receivership at both banks up until they were ultimately offered. (First Republic Bank likewise had a big quantity of uninsured deposits.)

Since billions of dollars in domestic uninsured deposits were at threat at the 2 banks that stopped working in March, federal regulators released a “ unique threat evaluation” that enabled the FDIC to cover all uninsured domestic deposits at those 2 banks. That action led to billions of dollars in additional losses to the FDIC’s Deposit Insurance coverage Fund (DIF).

To send out an alerting to the mega count on Wall Street about their own vulnerability to uninsured deposits, in addition to to cover the DIF’s losses, the FDIC launched a proposition on Might 11 to impose an unique evaluation based upon the specific bank’s holdings of uninsured deposits since December 31, 2022. The evaluation would total up to a charge of 0.125 percent of a bank’s uninsured deposits above $5 billion. The charge would be topped 8 quarters according to the proposition.

According to the 10-Q filing that JPMorgan Chase made with the SEC on August 3 for the quarter ending June 30, if the FDIC’s guideline is completed as proposed, “the Company anticipates to acknowledge an approximated evaluation cost of around $3 billion (pre-tax) in the quarter in which the guideline is completed, which is anticipated to happen in the 2nd half of 2023.”